Description

Suntory was founded in 1899 in Osaka, Japan. Suntory Beverage

and Food (TSE:2587) is a stable, conservatively financed, low revenue growth

(1-4% annually), beverage company with trademarks and prominent brand names.

Suntory’s acquisition of Ribena and Lucozade from GSK in

2012-2014 for 1.35B pounds, and previous purchases of Orangina and Schweppes

for 2.8B Euros in 2009— enhanced Suntory’s brand and share of mind.

Today, Suntory has more than 300 subsidiary companies, 38,000

employees with products in 50 countries. Don’t confuse Suntory’s alcoholic

segment, Beam Suntory (private), with Suntory F&B (public)

The high margin, private, alcoholic segment called Beam Suntory—

includes prominent brands such as Maker’s Mark, Jim Beam— comprising of 33% of

revenues for the entire holding company. This entire article is dedicated to

the non-alcoholic segment— Suntory F&B, which is public on the Tokyo stock

exchange.

Let me get this straight, right off the bat—Suntory will not become

another Coke—it will not reach the same scale as coke through geographic

expansion or additional marketing and branding, nor is the current beverage

industry as good as before, despite consolidation—competition has

intensified.

The majority of Suntory’s products are sold mainly to 8

countries under established brands such as Ribena, sports drink Lucozade, TEA+,

MyTea, GoodMood, Boss Coffee, Brand’s Chicken Essence, Orangina, etc.

However, Suntory is still a predictable business worth studying.

Suntory has tried experimenting with a carbonated version of

Ribena, and has come out with Lucozade with a lower sugar content— they changed

their ingredients and marketing to become more health conscious brand in

response to the imposed sugar tax in U.K and Thailand.

Despite having a 20% market share at home (Japan), owning most

of their vending machine distribution channel, and being a major supplier to

most convenient stores and groceries— Japan is a shrinking and saturated

market.

Major growth for Suntory will come from improving operations in

Europe (sports drinks and energy drinks) and working with Pepsi on their J.V in

Thailand and Vietnam (growth continues to be faster than other markets), the

United States (North Carolina), and New Zealand.

Business model and summary of financials

Compared to Coke, Suntory’s business is less reliant on bottlers

and franchisees. Coke does not import any of its ingredients— in

China, Coke has 2 franchisees/bottlers— COFCO and Swire, which sets

up a factory and gets Coke’s “proprietary” ingredients to produce— teas,

Gatorade, Coke, Vitamin Water, Fuze, etc. The parent company, then collects a

portion of these profits from bottlers. Distributors/Franchisees allow Coke to

be more asset light on the balance sheet. Suntory owns most of their factories.

Gross margins have dropped from 54% in 2015 to 41% in 2020. This

is not due to Suntory lowering their product price, but due to a decrease in

sales in the past 3 to 4 years while maintaining the same cost of goods sold.

Due to the pandemic, utilization rates were less than ideal at certain plants.

Over the last five years, operating margins have remained

stable, because SG&A lowered from 43% in 2015, to 32% in 2020. Suntory’s

management has indicated ideal EBIT margins to be 10%, and would like operating

income growth to be at double digits by 2023. Having an EBIT of 10% is

certainly possible, as 5 years ago in 2015, the EBIT was at 5-6%, and in 2020,

EBIT margins are near 7-8%.

Suntory is conservatively financed— in 2015, debt to equity was

70%. By lowering both short term and long term debt, debt to equity is now 23%.

Key factors to future success:

Success in carbonated beverages, energy drinks, teas, and

bottled water— boils down to—

1.

Pricing power & increasing sales volume

- If Suntory has pricing power, can it be

maintained through growth and acquisitions, or will competition deteriorate its

moat?

2.

Geographical locations- prospective size and growth

- How large of a market Suntory can capture

based on each country’s consumption per capita (different countries consume a

different amount of sugared water per person a year)?

-

Partly and indirectly

GDP per capita (disposable income to buy sugared water and other non-alcoholic

drinks)

3. How focused management is on delivering shareholder value.

- Improvement of existing product line

- If buybacks aren’t done, how else is

management producing value?

- Europe isn’t generate a high ROIC based on the

amount of assets…

Suntory has been working with retained earnings on the premise

that there probably won’t be buybacks in the future, and 25-30% of earnings

will be paid out as dividends and capital expenditures won’t be used to build

new factories in countries where Suntory doesn’t have an existing base within

the next 2 to 3 years.

Should Suntory reach USD 3-4B of free cash flow, it should be

worth at least USD 40-65B, or 4 to 5x its current price, as current market

capitalization as of February 2021 is approximately USD 10B.

Market Size for Energy Drinks and Carbonated Beverages

Globally, beverages form a significant industry—the sector has a

combined value of around USD 1.8-2T and 950B liters of drinks in consumption.

Packed water consumption exceeded 465 billion liters, making it the most

consumed type of beverage, with alcoholic beverages and carbonated beverages

ranked 2nd and 3rd. In terms of the

volume of annual consumption, non-alcoholic drinks make up 65%, including—

bottled water, carbonated drinks, soda, energy drinks, electrolyte drinks,

fruit juices, ready-to-drink tea and coffee, etc. Of this, almost half, or

160-210B, is generated from North and Latin America.

Suntory B&F, in terms of size, is the 4th to 5th largest in

retail value, but lags far behind Coke and Pepsi. U.S. beverage giant Coca-Cola

commands the largest share of the market, 20-25%, with PepsiCo holding 10-15%.

North America and South America dominate the global non-alcoholic beverage

market with a share of 25-33%. Suntory is weaker than Coke and Pepsi in

America, and also practically non-existent in China and India (except for Beam

Suntory, in which case Suntory’s alcoholic segment has entered these 2

countries).

Risks

1. In the U.S, the leading four manufacturers of carbonated drinks

had a concentrated market share of approximately 80%. The U.S is a stretch for

Suntory to expand in, and despite Suntory’s joint venture with Pepsi— the U.S

won’t be a major contributor to Suntory in the near future.

2. Suntory

has 20% market share in Japan, and is the 2nd place leader in

terms of market share, with Coke being number one. Japan is a shrinking market

which will be further discussed below.

3. How

far of a runway does Thailand and Vietnam bring? Remember, operations in the

United States and most of South East Asia is via a joint venture with Pepsi.

Europe also has a lot of fixing to do.

4. Steady declines in

carbonated soft drink volumes are largely due to health concerns, as soda's

high sugar and caffeine contents causes obvious health issues. Certain

countries like the U.K and Thailand, which Suntory has operations in, have

implemented a sugar tax, and Suntory is responding with healthier products.

The shifting trend towards healthier drinks—

In 2020, carbonated drinks only accounted for 20% of global

non-alcoholic drinks sales, compared to mineral and spring water at 60% and

fruit and vegetable juices at 20%. By volume, bottled water accounted for 24%

of all US beverages in 2017, versus 22.3% for second-place carbonated soft

drinks.

Still bottled water - spring, mineral and purified, carbonated

& flavored bottled water - are the 2nd highest retail value of soft drinks

with sales of 239B in 2019, representing growth of 33.4% or 60B since 2015.

This is why Coke’s purchase of Vitamin Water was a no brainer and why Suntory

is introducing ready to drink non-sweetened tea in Asia and Europe (MayTea).

Crucial Factors in measuring Suntory’s progress

From 2013-2020, in a span of 7 years, Suntory Beverage has

generated 670B yen, or USD 6B in cash flow by roughly employing 8T yen, or USD

80B of capital. This gives us a cumulative return on capital of 8% in the last

7 years.

Can Suntory generate 700B to 1T yen, or USD 7-10B, in the next

4-5 years? I sure think it is possible. Will aggregate growth be in double

digits? It seems unlikely.

The way to measure the potential is though GDP per Capita and

consumption per capita based on population size, and pricing power.

Pricing Power

Coke sells approximately 1.8 billion, 8oz servings, daily. In a

year, 657-660B, 8oz servings, are sold.

If you increase the price by a penny, you’ll get an additional

18 million dollars a day, which amounts to 6.57B dollars a year. With

trademarks and strong branding and marketing and a 127 year history, Coke is

able to get the consumer to pay an additional penny raised without decreasing

volume.

Does Suntory have the same pricing power? Yes, but not on the

same scale as Coke or Pepsi. Suntory’s non-alcoholic beverage division sells

approximately 17B 500ml bottles, which amounts to 35B 8oz servings annually.

Should Suntory raise its products by a penny, it brings in an

additional 350 million annually.

35B 8oz servings for Suntory vs. 660B 8oz servings for Coke

means that in terms of volume consumed annually, people consume Coke products

18 times more than Suntory's drinks.

Coke definitely has a scale advantage, and Suntory has not

expanded geographically to countries with the same population density to

provide the same long runway, but is still has a decent runway ahead.

To repeat myself to make a point— 6.57B dollars a year for

a penny raised and attests to Coke’s scale and marketing done to purchase a

share of mind over decades. This is a moat not easily replicated by

Suntory.

GDP per Capita

Soft drink consumption generally increases with income. Although GDP per capita is

often used as a broad measure of average living standards, high levels of GDP

per capita does not necessarily correlate with high levels of household

disposable income— a key measure of average material well-being of

people.

As a rough measure— a 10 times increase in per capita GDP was

associated with a 5 times increase in the annual number of gallons of soft

drinks consumed per person.

In the chart above, these are countries besides Japan which largely

affect Suntory’s bottom line. Vietnam will eventually catch up to Thailand, and

eventually, both countries will reach at least half of the GDP per capita of

Western European countries, it is just a matter of time.

In relation to total population figures, sales of non-alcoholic

beverages generated USD 52 per person in 2020.

Consumption per Capita

In 2021, globally, the average per capita consumption stands at

27.4L per person, or 6.5— 8oz servings per person. While this is the average,

different countries have vastly different consumption habits of non-alcoholic

drinks, making certain markets more lucrative. The idea that the potential

growth in any country could at least reach half the per capita consumption level

in the U.S. – is a perfectly reasonable estimate.

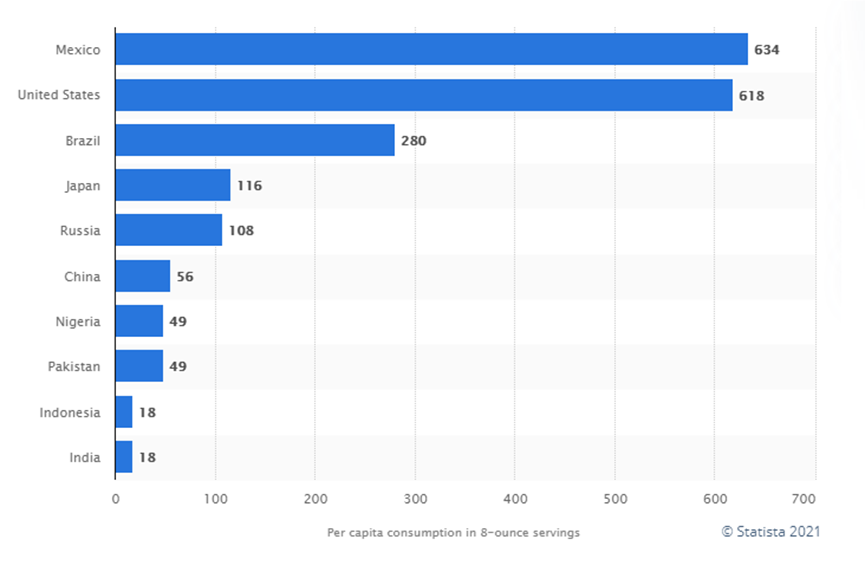

Here are the top 10 countries where people drink the most

8-ounce servings of Coca-Cola products per person per year:

Per capita consumption of carbonated soft drinks in 2019 in the

ten most populated countries worldwide (in 8-ounce servings)

With the charts above, and the key figures in consumption per

capita, we will now proceed to talk about each geographical region which plays

a big part in Suntory’s bottom line. As you can see in the top 10 most

populated countries with consumption per capita, Suntory is only in USA, Japan,

and Indonesia, with USA only being a surrogate, with Pepsi having all the power

and most of the profits in the partnership.

Regional Analysis: Dominant player at home (Japan, a shrinking

market)

Suntory is a dominant player domestically (Japan), boasting the

number two market share in Japan in terms volume, with Coke being number one.

Suntory has a 21% market share—per capita consumption is almost 3 to 5 times

that of other southeastern Asian countries, but Japan’s carbonated beverage

market is shrinking along with its population.

As of January 2021, Suntory’s year-on-year % change of Soft

Drinks sales volume in Japan was -9%. From January to June 2020, Suntory’s gross

profit in Japan decreased 19.1 billion yen (USD181.7M) mainly due to volume

decline and channel mix deterioration. Suntory will have to rely on

acquisitions and expansion in the Asia Pacific for growth.

The domestic market comprises almost half of Suntory’s total

revenue and 35-40% of operating profits. Suntory Tennensui (mineral water) and

Boss Coffee, makes up 50% of the domestic sales in terms of volume sold. In

addition Suntory is consolidating Japan Beverages’ sales branch, while growing

core brands— Suntory Tennensui, BOSS, and Iyemon with a primary focus on

branding them as healthy products. The coffee brand, Craft Boss is also

undergoing a major brand renewal.

In Japan, a large part of sales derives from Suntory’s vending

machines. As part of the agenda to counter shrinking domestic sales— installing

machines in the right locations with large working population to prevent sales

per machine from declining, and introducing larger machines to reduce refill

rates are crucial.

Due to the pandemic, vending machine sales roughly halved at one

point due to the stagnant traffic in April and May 2020, and operations were

inadequate to cover fixed costs. As of 2021, normal traffic (90%) resumed.

Regional Analysis: Asia – Vietnam and Thailand

Suntory entered developing markets such as Vietnam and Thailand

through joint ventures with Pepsi contributing to a runway for compounding and

growth. PepsiCo nearly tripled its business in emerging and developing markets

from 8B in annual revenue in 2006, to 22B in 2011.

One can argue these east Asian countries Suntory has production

in, are limited to a smaller population— Coke and Pepsi have a geographical

reach for countries such as China, India and even Africa, which has billions of

people, instead of millions like Vietnam (96M) and Thailand (70M).

Suntory’s revenue for Asia, which includes Vietnam, Thailand,

and Indonesia, was 212.0 billion yen (USD2B). Suntory expects revenue growth of

9.6% to 292 billion yen (USD2.8B) in Asia, which will be driven by core brands—

TEA+, Brandʼs Chicken Essence, V, and the energy drink, Sting.

South East Asia makes up 28-30% of Suntory’s total operating

profits. Asia’s profit for Suntory was 27.9 billion yen (USD265M). Suntory’s

target is to reach 37 billion yen, or 7.1% year-on-year growth.

Thailand makes up 28% of total revenues in Asia at 61.4B yen

(USD 584M), and Vietnam makes up 37% at 79.5B yen (USD 756M), the third part of

revenues comes from a health supplement called Brand’s Chicken Essence which is

popular in Asia. It comprises of 23% of total revenue at 48.6B yen (USD

462M).

While GDP per Capita is higher for Thailand than Vietnam, for

non-alcoholic beverages, data (see previous chart in consumption per capita)

suggests that Thailand also leads Vietnam by 108 liters per capita to 36.

However, due to Thailand’s sugar tax, when isolate soft drinks

as a category, in 2020, Vietnam’s consumption per capita for sweet drinks is

almost double of Thailand— with 55 Liters per capita for Vietnam, and 28 liters

per capita for Thailand.

Vietnam

Vietnam, had its ups and downs— the bottled water brand Aquafina

recorded double-digit volume growth, while Suntory’s TEA+, an oolong tea

product captured sales of 10 million cases and above, but sales of Suntory’s

Sting energy drink faltered. Suntory hopes to revive Sting sales with the

launch of a new product, as rival Red Bull has increased its market share with

the release of a lower-priced offering.

In Vietnam, there are roughly 135 manufacturing enterprises

churning out 7-8billion liters of non-alcoholic beverages annually at a growth

rate of roughly 6-8% which roughly translates to 85T VND of industry sales

(3.67B). Beverage consumption is around 90-100B liters in 2020 according to

EVBN report. Off-trade is a sales channel (such as supermarkets and groceries)

accounts for about 60% of the non-alcoholic beverage market, while the

remaining 40% is represented by products are directly sold at restaurants,

eateries, etc.

Pepsi entered the Vietnam market in 1994, with only Pepsi and

7-up, and has since invested more than 500 million in five beverage

manufacturing plants in Vietnam, a high priority for Pepsi's aggressive

development in emerging markets. Today, there are more than 13 beverage brands.

Suntory created a joint venture with Pepsi after 2010. Coca-Cola

and Pepsi were being questioned about the price transfer by local tax

authorities since they both recorded huge losses for a long time. When

significant profitability occurred in 2017, Pepsi erased losses with an

accumulated profit of VND 2,735 billion (USD117M). Suntory PepsiCo Vietnam

recently recorded accumulated profits over 150M.

Pepsi has in recent years outperformed Coke with double their

revenues. Specifically, in 2017, Pepsi achieved a revenue of VND15

trillion (645 million) and an after-tax profit of VND 1.42T (61.3 million), up

5% and 27% respectively compared to 2016.

Coca-Cola’s revenue in Vietnam grew at 6% in 2017, reaching VND

7.2T (310 million). However, due to steep increase in costs, Coke had a net

profit of VND 227B (9.75 million)— half of previous years. Coca-Cola has

reduced about VND 1 trillion (43 million) in accumulated losses thanks to its

accumulated profits in recent years. Competitor Coca-Cola recently received

approval from Vietnamese authority to establish a new 300 million production

facility in Hanoi, its 4th in the country to produce beverages such as

Coca-Cola, Fanta, and Schweppes and Fuze Tea.

The four biggest names in Vietnam’s non-alcoholic beverage

market include Coca-Cola Vietnam, Suntory PepsiCo, URC Vietnam from the

Philippines, and Vietnam’s Tan Hiep Phat.

Suntory-Pepsi and Coca-Cola’s biggest local rival is Tan Hiep

Phat, which is leading the green tea segment with Zero-Degree Lemon Green Tea

and Dr. Thanh products.

According to Euromonitor’s report, the non-alcoholic beverage

market share in Vietnam based on PepsiCo's off-trade sales has risen sharply

from 27% to 33% in the past five years.

Meanwhile, that of Coca-Cola was only around 10-11% and Tan Hiep

Phat was down from 16.5% to 13.1%.

Thailand

Thailand's soft drinks market is estimated to be worth 800 billion yen (USD7.5B) in retail sales. According to Nielsen, the carbonated soft drink industry in Thailand was estimated to be worth 56 billion baht (USD1.85B) in 2019, up 12% over the previous year. Of the total carbonated soft drink industry, 71% belonged to cola drinks, 23% flavored drinks and the remaining 6% to the lemon-lime segment.

In order to create a joint-venture in Thailand, Suntory paid 33

billion yen (USD289M) to acquire a 51% stake in Pepsi’s International

Refreshment. Suntory PepsiCo Beverage Thailand was established to expand sales

of non-alcoholic drinks in the standard categories of carbonated drinks,

bottled water, electrolyte drinks, ready-to-drink tea and coffee, and fruit

juices.

At 42 liters per capita consumption for carbonated drinks, and

12-15% year on year growth, Thailand’s future for carbonated beverages may look

bright, but for many years domestic demand has been weakening. Continuous

double digit growth may not be sustainable, as shifting concerns with health

and growing competition from local drinks manufacturers such as Thai Beverage.

In the last five years – 2012 through 2018 – Suntory & PepsiCo invested

hundreds of millions of US dollars in Thailand in two beverages and two foods

manufacturing plants. PepsiCo invested in its first beverage plant in Thailand,

located in Amata City Industrial Estate of Rayong Province in 2012.

In 2016, Suntory Pepsi opened a beverage plant in Thailand,

located in Nong Khae Industrial Estate, Saraburi Province, with an aim to

double the capacity of its first plant.

In 2018, PepsiCo and Suntory established new distribution routes

for goods through the Deutsche Post—DHL Group. At the same time, a network of

sales agents were placed across the country in hope that more drinks will be

sold at national retailers.

The collection of taxes in Thailand on drinks according to sugar

content has brought about changes—Suntory raised their pricing in water and

tea, and ingredients were aligned to avoid the sugar tax in beverages. In

response to this, Suntory adjusted their production processes to reduce

carbonated drinks’ sugar content and to use non-sugar sweeteners instead (with

an accompanying cut in tax of THB 0.25-0.36 per bottle). Initially, the tax

rates were set at a relatively low level but were increased every two years up

until 2023.

Tea and coffee are tax-exempt from the list because they count

as agricultural products beneficial to health. In 2017 to 2020, consumption of

carbonated drinks continued to fall, shrinking by 3.2% YoY. This is especially

serious for carbonated drinks, which typically have a high sugar content (taxes

added THB 0.13-0.50 per bottle).

For the health supplement business, Bird’s Nest continues to be

a non-performer, while Brand’s Chicken essence sales were especially strong in

Thailand, rising 10% this year due to a better distribution strategy. Suntory

also continued boosting marketing efforts for low to zero sugar Pepsi, and by

investing more into the TEA+ brand.

Regional Analysis: Europe— France, U.K, Spain

In Europe, Suntory’s main focus is in France (population: 65M),

Spain (45M), the United Kingdom (65M). The European segment also includes

Italy, Northern Europe, and Africa. Revenue was 190 billion yen

(USD1.8B). Segment profit was 27.2 billion yen (USD255M).

In 2009, Suntory acquired the Orangina Schweppes Group, which

today manufactures and sells carbonated beverages (Orangina, Schweppes, etc.)

and fruit juices (Oasis) in Europe. In 2013, SBF acquired the Lucozade and

Ribena beverage brands from GSK.

Suntory expects further unit price deterioration in 2021 for

Europe and a turn for the better in the next 3 years will require a push in new

products and control costs.

In terms of the European segment, of the 190B yen in revenue

from Europe, France and Belgium contributed to 86.6B yen (45% of sales), U.K

and Ireland contributed to 54.1B yen (28% of sales), while Spain and Portugal

contributed to 31.2B yen (16% of sales). France and Belgium are by far the

biggest contributor to the European sales segment. Suntory expects revenue

growth of 12.3% to 222.0 billion yen through brand expansion of Schweppes

across Europe.

France

Orangina was acquired by Suntory in 2009. Suntory now has six

major flagship brands in France— Orangina, Schweppes, Oasis, Pulco, Champomy

and Maytea. In France, Suntory has revitalized its Oasis brand, and thoroughly

strengthened marketing activities for Orangina, to maximize both revenue and

profit.

Suntory’s MayTea brand has become Suntory’s second-biggest brand

in the French bottled tea market only two years after its launch and will be

introduced to other European countries.

As the leader regarding fruit drinks in France with 20% market

share (2019) and four production sites in France –La Courneuve, Meyzieu,

Donnery and Châteauneuf-de-Gadagne— Suntory is one of the top players in the

beverage segment with a 908 million euro turnover (2019) and a consumer base of

17 million households in France. In France, Orangina and Oasis performed much

better than the market especially in the summer of 2019.

Suntory’s capital expenditures in France include upgrades at

Suntory’s Orangina plant in Meyzieu— with an accumulation and packaging

solution (GeboAQFlex, and Sidel’s Aseptic Combi Predispenser) that covers a

wide range diverse bottle shapes and sizes –nine various bottle formats from

0.2 to 1 Liters, including square bottles to which traditional mass

accumulation solutions are not suited— fully respecting fragile and lightweight

containers for four brands – Oasis, Pulco, Maytea and O’verger.

This upgrade has immensely contributed in preserving Orangina’s

product quality with smooth, all-in-one, and contactless, single-lane product

handling. The accumulation solution also cover a wide range of outputs from

27,000 to 45,000 bottles per hour and provide extensive buffer capacity from 3

to 5 minutes of net accumulation to secure the overall line efficiency.

United Kingdom

In the UK, Suntory is trying to market Lucozade Sport for

sporting occasions, while maintaining the sales of Lucozade Energy. Lucozade

Energy trended steadily in 2020, resulting in better results than 2019. Suntory

is rolling out sugarless and carbonated versions of Ribena to preempt the

proposed introduction of the sugar tax. It seems some consumers have been less

than impressed as YoY sales declines of 1- 2%.

Suntory’s USD16M investment in a factory bottling line in

Coleford, Gloucestershire uses 40% less water and energy— resulting in an

aggregate 15% water reduction across all U.K plants. The Coleford factory

produces a billion bottles of Lucozade and Ribena a year.

Spain

Schweppes’s brand is a market leader in Spain, with a 55% share,

and has strong sales in tonic water due to gin and tonic’s popularity in

Europe.

In 2014, Suntory filed a lawsuit against Coke

for selling Schweppes tonic water made in the UK which was imported into

Spain. From 2009 to 2014,

17.3 million bottles were sold by Coke just by importing Schweppes from the U.K

to Spain at a lower price which gave Coke a 6 million pound profit. Coke argued that as they had

the rights to distribute the product in the UK, they had the same rights to

distribute it throughout Europe, but the court ruled against this. Suntory now

has the competitive advantage by being the sole owner of the Schweppes brand in

Spain.

With Spain having such a high consumption per capita, should

Suntory grow sales in Spain through its Schweppes brand and introduce other

drinks to penetrate further in the market, this could prove instrumental in

growing their European segment. Of the 1.2B liters of beverages sold in Europe,

Spain only makes up 16% of sales, or 134M liters. I understand both U.K and

France have a population around 65M, while Spain has a smaller population at

45M, but Spain can be a major contributor to operating profits.

Valuation

With a clean balance sheet and 30% debt to equity, selling at

12B enterprise value—

Suntory generates approximately 1B of free cash flow annually,

while growing revenue in low single digits. My conservative assumptions of

intrinsic value is at least 25-40B.

Suntory still has room for international expansion. Currently,

45-50% of its sales from abroad and further expansion should help with the

stagnant growth within Japan. Management has indicated future acquisitions will

be in Southeast Asia.

20-30% of Suntory’s free cash flow will be paid out as

dividends. Management mentioned in earnings calls that they forecast a revenue

of 2.5T yen by 2030 and they hope to return to a level of operating income of

115B yen or USD1B. As of 2020, revenue was 1.1-1.2T. This implies a CAGR of

7-8%.

Charlie Munger wrote an essay in 1996 explaining why Coca Cola

ought to be a 2 trillion dollar enterprise from 2 million dollars over a time

period of 150 years, which roughly translates into a compounded annual growth

rate of 9-10%.— “Practical Thought on Practical Thought”.

As mentioned before, coke is now worth 250B. Assuming Charlie

misses his target and coke is only worth 1 trillion by 2030, that’s a gain of

4x in 10 years (assuming we start from 2020). A doubling in 5 years,

corresponds to an annual rate of return of 15%.

As of February 2021, Coca Cola is worth an enterprise value of

approximately 240B while generating 8B of free cash flow, which gives it a

multiple of roughly 30 times. Pepsi, has an enterprise value of 220B, with free

cash flow of 6B. Pepsi and Coca Cola lead the market share in terms of soft

drinks, but Pepsi has to generate double the sales of Coke, since they are in

the low margin business of snacks and chips.

In a decade, it should be feasible for Suntory to be at

least worth 40B, should it improve its international portfolio as the

Japanese market shrinks.

When Coke was generating free cash flow of 1-2 billion dollars

in 1988-1994, its market cap was around 25-50B dollars. Right now, Suntory is

selling at a bargain price of 10-12B dollars.

Under realistic assumptions, I think in the next decade, at the

very least, by 2030, 2.5 Trillion yen (23 Billion USD) sales by 2030, will be

achieved by Suntory.

Is Suntory going to turn into another Coke or Pepsi? Does it

have a moat as strong as these 2 companies? No. I would argue its runway isn’t

even as long as Coke or Pepsi for compounding.

But in terms of valuation, for a company with such a healthy

balance sheet, it is undervalued.

I do not hold a

position with the issuer such as employment, directorship, or consultancy.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

- Improvements in factory efficiency and new products (Maytea) in U.K & France will be felt 1-2 years later

- Exclusive producer of the Schweppes brand in Spain, which has a high consumption per capita

- For Thailand, Chicken Essence and other beverage types may replace the slow down in carbonated beverages for double digit growth

- For Vietnam, bottled water and Tea+ products replacing the slow down in energy drink Sting

- For the domestic market (Japan), maintaining the dominance of having a 20% market share and finding ways to prevent shrinking consumption

- The market realizing for such a beverage company that utilizes very little leverage and having such brand names, should be worth a whole lot more than 12B,

- If Suntory were listed in the U.S, it would be at least worth 35B. Suntory can close the cash flow gap with Monster Beverage, but still may not realize an enterprise value of 46B....

I would highly recommend Mr Pedro loan services to any person in need of financial help and they will keep you on top of high directories for any further needs. Once again I commend yourself and your staff for extraordinary service and customer service, as this is a great asset to your company and a pleasant experience to borrowers such as myself. Wishing you all the best for the future.Mr, Pedro is the best way to get an easy loan,here is their email.. pedroloanss@gmail.com Thank You for helping me with loan once again in my sincerely heart I'm forever grateful.

ReplyDelete