https://www.maynardkeynes.org/keynes-the-investor.html

-John Maynard Keynes, whose brilliance as a practicing investor matched his brilliance in thought, wrote a letter to a business associate, F. C. Scott, on August 15, 1934 that says it all:

"As time goes on, I get more and more convinced that the right method

in investment is to put fairly large sums into enterprises

which one thinks one knows something about and in the

management of which one thoroughly believes.

It is a mistake to think that one limits one's risk by spreading too much between enterprises about which one knows little and has no reason for special confidence. . . . One's knowledge and experience are definitely limited and there are seldom more than two or three enterprises at any given time in which I personally feel myself entitled to put full confidence."

-While managing the Chest fund, Keynes grew to favor of making long-term

investments in companies whose balance sheets impressed him and whose prospects

for future business looked good.

-He believed that careful analysis of a company

was more valuable than inside information.

“the dealers on Wall Street could make huge fortunes

if only they had no inside information”.

-The investment strategy Keynes finally adopted is, in many respects, remarkably

similar to Warren Buffett’s.

-Buffett has acknowledged Keynes’s influence on his thinking.

-In 1991 he said Keynes was a man,

“whose brilliance as a practicing investor matched his brilliance in thought.”

Like Buffett, Keynes was sometimes criticised for investing in stocks he believedwould prosper in the longer term and then sticking doggedly with his selectionsdespite shorter-term problems.

Increasingly, Keynes grew to favor a contrarian style of investing, writing in 1937:

“It is the one sphere of life and activity where victory,

security and success is always to the minority

and never to the majority.

When you find any one agreeing with you, change your mind.

When I can persuade the Board of my Insurance Company

to buy a share, that, I am learning from experience,

is the right moment for selling it.”

Benjamin Graham later summarized the contrarian credo:

Mr Market comes along each day quoting you a variety of prices for assets.

He will buy or sell at the quoted price. Often his quotes reflect fair value. Mr Market is, however, a manic depressive.

On some occasions he is depressed and he prices assets too cheaply. Other days he’s unreasonably optimistic and his prices are too high. The contrarian’s job is to go investing when Mr. Market

is depressed and to divest when he’s unreasonably optimistic.

- In 1938, Keynes wrote his manifesto for sound investing using a concentrated,

balanced portfolio. He proposed:

1. A careful selection of a few investments (or a few types of investment)

having regard to their cheapness in relation to their probable actual

and potential intrinsic value over a period of years ahead and in relation

to alternative investments at the time;

2. A steadfast holding of these in fairly large units through thick and thin,

perhaps for several years, until either they have fulfilled their promise

or it is evident that they were purchased on a mistake;

3. A balanced investment position, i.e., a variety of risks

in spite of individual holdings being large,

and if possible, opposed risks.

His view of investing versus speculation was:

“Investing is an activity of forecasting the yield

over the life of the asset; speculation is the activity of forecasting

the psychology of the market.”

Keynes came to view too much speculative activity as economically damaging,

famously saying:

“Speculators may do no harm as bubbles on a steady stream of

enterprise. But the position is serious when enterprise becomes the bubble

on a whirlpool of speculation.

When the capital development of a country

becomes a by-product of the activities of a casino,

the job is likely to be ill-done.”

Keynes’s biographer, H.F. Harrod, summarised Keynes’s investing

philosophy with the words:

“He selected investments with great care and boldly

adhered to what he had chosen through evil days.”

Keynes became first bursar of King’s in 1924, taking on responsibility for

the college’s financial well being. He decided to concentrate all of the

college’s resources over which he had discretion into a fund called the Chest.

He intended using his trading and investing skills to considerably increase

the Chest Fund’s value.

His policy of selling properties and using the proceeds to

“speculate in the stock market” was opposed by many of

King’s College’s fellows.

1. Keynes’s view was that he would rather be a “speculator”

in an asset that had a daily price quotation and was liquid

enough to be bought and sold than an “investor” in something

whose price was largely unknown.

2. Keynes knew it would be imprudent to speculate with the

college’s money as boldly as he had with his own,

particularly with regard to high margin speculation.

3. Nevertheless he continued to invest in an aggressive manner,

leading to impressive but volatile capital growth in the Chest Fund.

4. His investing philosophy changed over time as Keynes

began to doubt his initial belief that he

could profit from his broad understanding of economic cycles.

5. He grew to favor making large investments in individual businesses;

Keynes was a logical man and individual businesses had balance sheets

he could study and they sold products or services whose value

he believed he could assess objectively.

Keynes spent half an hour each day on stock market research –

in the morning, still in bed – studying company reports,

reading the financial sections of the newspapers and speaking to his

various brokers by telephone.

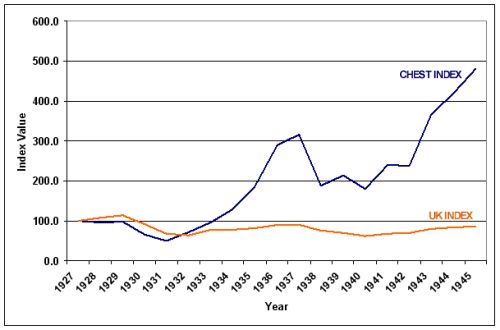

The Chest’s initial capital was £30,000. By the time Keynes died

in 1946 the fund had grown to £380,000 – an annual compounding

rate of just over 12 per cent. This might not seem very remarkable

but for the facts that:

-This performance was achieved during a period that encompassed

both the crash of 1929 and the build up to World War Two,

both of which proved disastrous for British stocks.

-In the same period of time, the British stock market fell 15 per cent.

The growth in the value of the Chest Fund was entirely

due to capital appreciation.

-There was no dividend reinvestment because Keynes

spent all of the dividends on the college. He believed the fund

was there to provide money for the college and was scornful of the

way other Cambridge colleges managed their finances,

referring to them as “savings banks”.

The performance of Keynes’s fund from 1927 to 1946 is shown below.

During these years the Chest grew at an annual compounding rate of

9.1 per cent while the general British stock market fell at an

annual compounding rate of slightly under 1 per cent.

R.F. Harrod – The Life Of John Maynard Keynes, 1951

William T. Ziemba – Hedge Fund Strategies, Performance, Risk and Disasters and their Prevention, 2004

Mark Harrison – The Empowered Investor, 2002

John Maynard Keynes – The General Theory of Employment, Interest and Money, 1936

Robert G. Hagstrom – The Essential Buffett;

Timeless Principles For The New Economy

Robert Skidelsky – John Maynard Keynes 1883 – 1946, 2003

Warren Buffett – Letter To the Shareholders of Berkshire Hathaway Inc., 1991

No comments:

Post a Comment